Local banks and credit unions are the backbone of America’s financial ecosystem, providing critical access to capital for small businesses and consumers. Despite holding less than 15% of total banking assets, these institutions are responsible for over 60% of small business loans and 77% of agricultural loans nationwide, according to the FDIC. Their impact outsizes their asset size—fueling local economies, fostering entrepreneurship, and keeping communities financially resilient. At the core of every community and regional financial institution is the delicate balance between lending and deposits. These inefficiencies impact borrowers and they limit growth potential, increase compliance risks, and reduce operational effectiveness. Without modernizing their lending infrastructure, many local institutions risk losing their competitive edge and missing out on critical revenue opportunities.

Strengthening communities through efficient lending

The loan-to-deposit ratio (LDR) is a crucial metric that determines how effectively an institution is using its deposits to generate revenue while maintaining the liquidity needed to meet withdrawal demands. Striking the right balance allows banks and credit unions to drive economic growth while ensuring long-term financial stability.

But growth in lending must be carefully managed. While increasing loan volume fuels profitability and supports local economies, it also increases exposure to credit risk and potential defaults. Effective risk management—through modern underwriting technology, including alternative credit data, robust fraud prevention measures, and the tools to enable data-driven decision-making—is essential to maintaining a healthy loan portfolio.

Lending is a fundamental driver of liquidity. In fact, 92% of deposits in the banking system are sourced from funding liquidity created by lending. This underscores how closely tied deposit growth and lending success truly are. When banks and credit unions have efficient lending processes, they don’t just strengthen their own institutions; they strengthen the communities they serve.

The high cost of legacy lending technology

Despite their vital role in the economy, banks and credit unions face significant challenges in a rapidly evolving financial landscape. Large, resource-rich megabanks that are heavily investing in advanced digital lending capabilities, and venture-backed neobanks that have optimized for a tech-savvy consumer experience are both significant threats, giving them a competitive edge in attracting and retaining borrowers.

At the same time, customer expectations have shifted. The demand for instant, frictionless financial services has never been higher. Borrowers expect fast, digital-first experiences—whether they’re applying for a personal loan, securing an auto loan, or obtaining capital for their small business.

Yet, many community and regional institutions still rely on outdated, manual lending processes that slow them down and create unnecessary friction for both their employees and their borrowers. Traditional lending process struggle with:

- Lengthy, complex loan origination workflows that cause employee and customer friction and introduce numerous opportunities for human error

- Lack of automation puts burden on employees and delays distribution of funds creating a poor borrower experience

- Outdated fraud prevention measures that increase risk exposure

- Disconnected customer experiences that create borrower frustration and limit engagement

- Limited ability to accurately assess and manage default risk while scaling loan volume

These inefficiencies impact borrowers as well as limit growth potential, increase compliance risks, and reduce operational effectiveness. Without modernizing their lending infrastructure, many institutions risk losing their competitive edge and missing out on critical revenue opportunities.

The Path Forward: A Digital-First Lending Strategy

To stay competitive, banks and credit unions need a modern, fully digital loan origination solution that allows them to seamlessly originate loans and deliver funds quickly and easily to customers. Financial institutions need technology that automates compliance checks (KYC, AML) and underwriting to expedite decisions while maintaining risk standards. They also need a data-driven way to identify and offer cross-sell opportunities to deepen customer relationships and increase wallet share. By leveraging automation and real-time analytics, banks and credit unions can scale lending without sacrificing the credit quality and stability that safeguard their long-term success.

Customers expect their banking needs to be met instantaneously, so financial institutions need a way to deliver funds to customers immediately after loan offers are accepted. Modern systems still need to integrate seamlessly with traditional core banking systems in real-time to ensure accurate and updated information across systems. Overall, adopting the right loan origination technology leads to a faster, more efficient, and customer-centric lending experience that builds upon the principles of relationship banking while ensuring compliance and risk management.

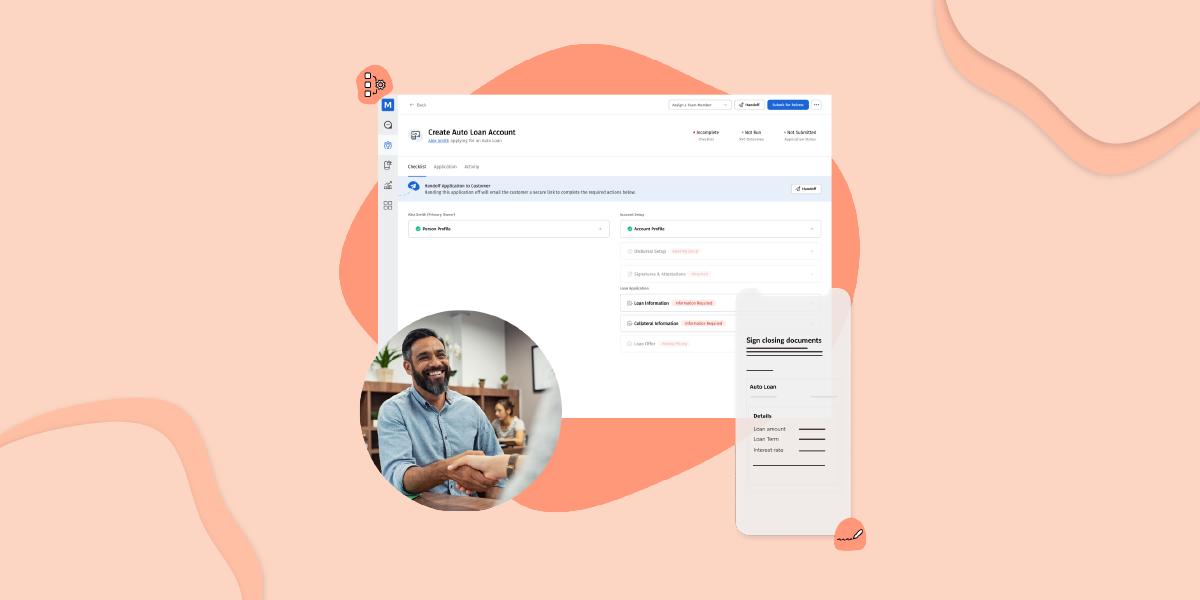

MANTL’s Solution:

MANTL Loan Origination accelerates growth for banks and credit unions by delivering seamless digital application and document management, unmatched automation, streamlined eligibility verification and memberization, and an exceptional customer and employee experience.

MANTL Loan Origination offers:

- Fully Integrated Loan Origination System (LOS): Streamline and simplify the entire loan process from application to booking to increase back-office efficiency.

- End-to-End Digital Lending Experience: Allow borrowers to apply, review approval, sign, and fund loans digitally, improving borrower convenience and satisfaction.

- Automated KYC and AML: Ensure regulatory compliance while minimizing manual review to reduce fraud and free up staff time.

- Real-Time Decision Engine: Enable fast, data-driven loan decisions to provide instant preapproval and speed up the loan process.

- Automated Eligibility Verification and Memberization: Seamlessly verify membership eligibility and automatically creates memberships and primary shares within the account opening workflow.

- Advanced Cross-Sell Capabilities across Loans and Deposits: Provide targeted offers in real-time to increase customer value and build loyalty.

- Real-Time Analytics and Reporting: Access customer and loan performance data to drive data-driven decisions and optimize strategy.

Winning the Future of Lending

Lending is the foundation of banking. But to continue thriving in a competitive financial landscape, banks and credit unions must embrace modern, digital-first lending solutions that enhance efficiency, improve customer experience, and drive revenue growth.

With MANTL Loan Origination, community and regional institutions can bridge the technology gap, compete with megabanks, and deliver the fast, seamless lending experiences that customers expect—without sacrificing the personal, relationship-driven service that sets them apart.

Now is the time to modernize lending. Are you ready to transform your loan origination process and unlock new growth opportunities? Contact us to learn more.