Read the original article here.

When Patrick Sells took up his role of chief innovation officer at Quontic Bank two years ago, he had to quickly figure out a fix for a major problem on his hands.

Quontic, a community bank based in New York City, was facing pressure from the Office of the Comptroller of the Currency to increase its deposits since its balance sheet was composed of 70% brokered deposits. It decided to pursue the route of becoming a digital bank to grow its core deposits, but it quickly discovered the onboarding process was turning prospective customers off. About 80% of prospects were abandoning their efforts to sign up.

“We were hearing negative reviews from people, a lot of people were bouncing, and it was just incredibly expensive [to acquire customers],” he said. “We decided to do something, and in particular, where basic online account-opening technologies really struggle is knowing who your customer is.”

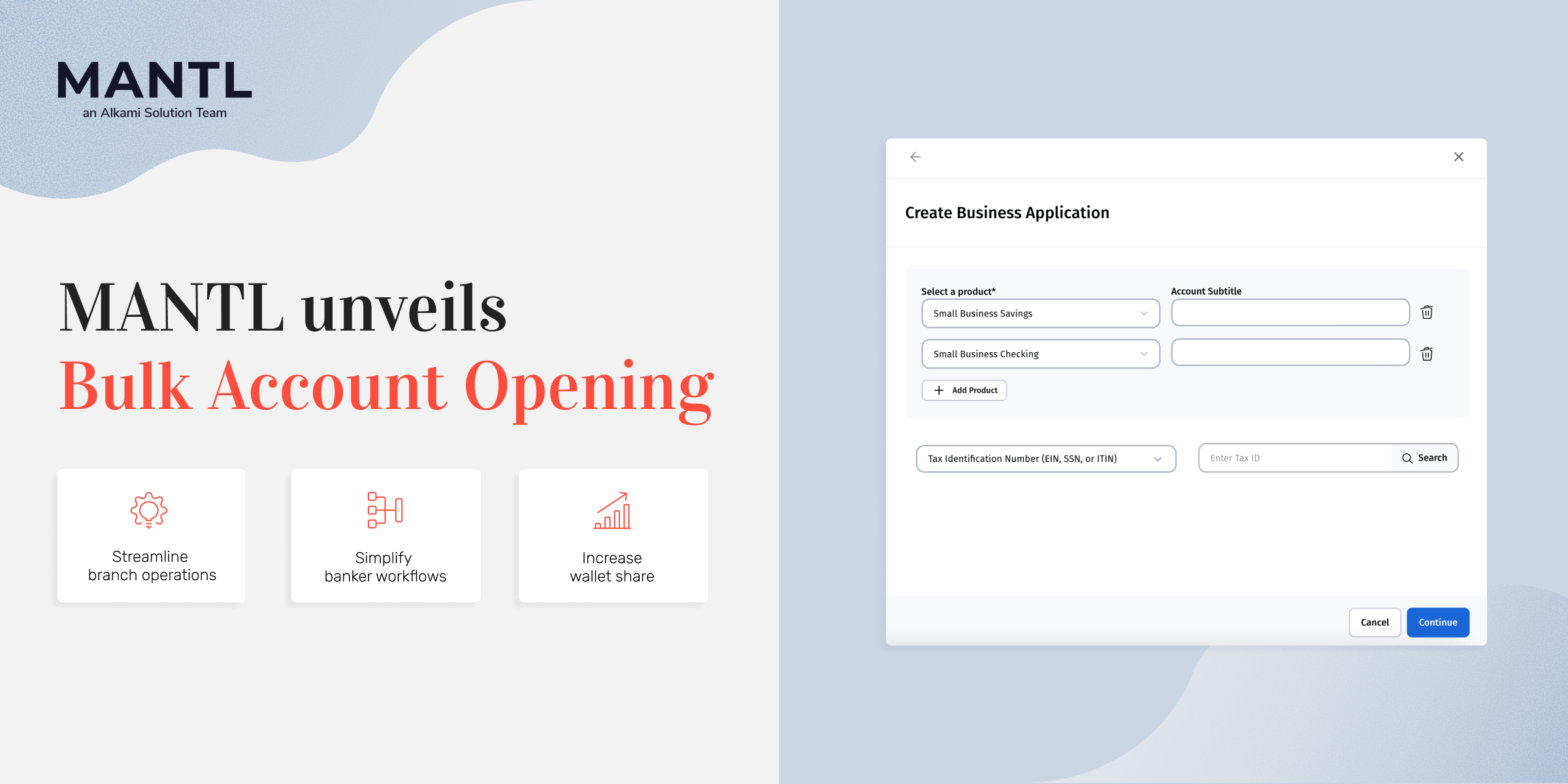

After experimenting with some account-opening tools, in April of this year, Quontic decided to partner with MANTL, a tech company whose account-opening solution serves community banks and credit unions. Sells said MANTL helped more than double its asset base — from $417 million in assets in March to $1.2 billion today — and checking accounts are now 83% of Quontic’s new accounts.

MANTL’s sweet spot: Speed and ease of account onboarding

MANTL, a 4-year-old company based in New York, initially sought to create a challenger banking brand of its own, but in its second year of operations, it pivoted to a B2B model, helping community financial institutions keep pace with digital transformation spearheaded by fintechs and large incumbents.

“Ninety-five percent of community and regional banks outsource their technology to third-party vendors like FIS, Fiserv and Jack Henry,” MANTL CEO Nathaniel Harley told FinLedger.

“The missing piece was, how do we enhance the bank’s core banking system, and how do we provide them with a fintech-like experience so they truly serve their customers better.”

Harley contends that among the largely brick-and-mortar community bank segment, 20% offer online account opening, and they typically lose 80% of customers during complicated sign-up processes that rely on the review of documents, which could include driver’s licenses or passports.

By contrast, MANTL’s identity verification process uses automated non-document verification techniques that may involve a customer offering their social security number. In turn, the customer’s details are cross-checked with publicly-available databases, and information from reporting agencies or other data sources.

“MANTL integrates with a number of underlying KYC [know your customer] and AML [anti-money laundering] data sources that are verified information that the end customer is entering,” Harley said. “There’s a higher statistical probability that we’re able to know who they say they are, without needing to collect a document.”

The streamlined account sign-up process saves minutes of precious time and onboarding clicks, Harley explained, reducing sign-up times to two minutes and 37 seconds, or 24 clicks. That compares to 10 minutes, or 60 clicks, using Quontic’s legacy account-opening system.

MANTL’s other clients also report impressive results using the company’s tools: Midwest Bank Centre, which had no digital solution prior to MANTL, raised more than $180 million in deposits since going live with MANTL in 2019, and Cross River Bank raised $250 million in 15 days in April 2020 through certificates of deposit, with an average deposit of more than $137,000.

MANTL’s roadmap

As of the second quarter of this year, MANTL has grown client deposits by 705%. The company has raised $20.7 million, including a $19 million Series A round it concluded in June, resources it said it would devote toward reducing its 90-day time-to-market and helping clients launch new products.

Asked whether the company is interested in expanding the reach of its tools to other types of institutions, Harley said he believes there is still significant runway for growth within the community banking and credit union sectors.

“For now, we’re really happy to be focused on the sort of middle-market community regional banking and credit union segment,” he said. “We are just naturally getting pulled more upstream as we continue to grow the business, but I think there is a lot of opportunity just within the segments that we are going after.”

On the client side, one possible area for expansion is institutions that serve business customers.

“There is a wide open need for business and commercial onboarding and account opening,” he said. “Twenty percent of banks have online account opening for consumers, but it’s less than 1%. on the business side.”

For Sells, a key appeal of the MANTL solution is the ease with which it can work alongside existing core banking technology platforms. He contends that getting the account onboarding process right is crucial, because it sets a service benchmark from the beginning.

“When that first experience with your bank online sucks, that sets the tone through which the customer is going to grade everything else you do,” he said. “We have to have the best experience possible when someone comes in. It needs to be as easy as ordering an Uber.”

Late last month, FinLedger reported on a warning from the chairwoman of the FDIC that “even well-capitalized, well-managed community banks will not survive if they fail to adopt technology that fintech companies and large banks already offer.”