See the original article here.

Less than six months into his job as chief innovation officer at Quontic Bank, Patrick Sells was stymied.

Steven Schnall, Quontic’s chairman and chief executive, had persuaded Sells to give up his work as an independent marketing consultant and come on board to revamp the New York bank’s digital efforts — everything from operations to the customer experience.

The challenge of helping Quontic grow from a small community development financial institution under the pall of regulatory scrutiny into a thriving digital innovator had Sells excited. But the staff seemed to balk at his every effort to implement new technology and change processes.

“There have been many times when I just wanted to pull my hair out,” Sells said.

He understands now why there was such resistance. After all, he is a 29-year-old new to banking, a complex industry with a steep learning curve. “Here we are trying to do something fundamentally different, and I didn’t understand the language of bankers,” he said. “I was just frustrated beyond belief they just didn’t seem to get that it’s OK to have some mistakes.”

The pressure was on to increase core deposits, under a freshly inked agreement with the Office of the Comptroller of the Currency. The OCC had deemed Quontic — which is headquartered in Manhattan, but has a single branch in Astoria, and focuses almost exclusively on mortgage lending — too dependent on wholesale funding.

Sells joined the bank in October 2018, the same month the agreement had been signed.

Just a few months later, the bank had started to make improvements by enabling new customers, for the first time, to sign up online for its deposit products.

But even as friction on the customer side diminished, it ratcheted up internally. “I was wanting to keep pushing on the next round of what we were going to do. But they’re just like, ‘Patrick, we can’t do this,’” Sells said.

“Banks can absolutely be innovative,” says Quontic Bank’s Patrick Sells. “There’s no reason what you see a fintech doing you couldn’t do yourself.”

In his view, the problem wasn’t the “percent of a percent of a percent” of fraud that had cropped up during the influx of account openings, as his colleagues were saying. It was entrenched thinking.

“I just remember being blue in the face trying to explain this,” Sells said.

Adopting new technology and trying out new tactics was well within Sells’ comfort zone. He had started running his own digital marketing firm at the age of 21. But to cautious bankers, the changes happening at Quontic felt jarring.

Even more, the fear of getting something wrong was paralyzing, Sells realized. It kept the staff from wanting to try anything new.

“That’s when the antidote of ‘a policy of failure’ crystallized,” he said.

Sells told them, “We’re going to come up with a policy that says we are OK with failed technology up to this many dollars.”

It was a shift in thinking that paved the way for future tech upgrades on many fronts. His team went on to roll out three-minute account sign-ups and began running application programming interfaces, or APIs, in-house with a custom-built database in the cloud — the stuff of big banks and fintechs.

This groundwork turned out to be fortuitous for Quontic as the coronavirus crisis raged. With some speedy teamwork, Quontic managed to get involved in the Small Business Administration’s Paycheck Protection Program, by providing liquidity support for fintech lenders such as Intuit and Square. Though the overall volume of loans turned out to be less than Sells hoped, he said the satisfaction of pitching in to help some businesses survive the economic fallout of the pandemic justified those frenzied nights and weekends in April.

Sells, now unabashedly enthusiastic about what lies ahead, sees a future where Quontic customers transact with wearable tech and can opt for a deposit product with ties to cryptocurrency if regulators give their blessing.

“I think one of the things that community banks are doing poorly is we’re letting fintechs create a lot innovation for us — or they’re creating a lot of innovation because we’re slow,” Sells says. “And then banks feel like, ‘We’re not innovative, so we’ve got to partner.’ Well, no; banks can absolutely be innovative. There’s no reason what you see a fintech doing you couldn’t do yourself.”

To many within Quontic, Sells’ self-described “pontificating” sounded crazy early on. But with the endurance of the ultra-marathoner that he is, a steady campaign of kind persistence informed by years of studying business gurus, and Schnall’s support, Sells has won them over to the idea that there is no reason for Quontic — or any community bank, for that matter — to be a laggard in the tech space.

For creating the road map to help Quontic in its transformation, Sells is being recognized as our Digital Banker of the Year.

Hearts and minds

Sells began working with Quontic as an independent contractor in February 2018, devising digital marketing strategy for the bank’s reverse mortgage business and helping integrate customer relationship management technology into its process.

Schnall said he soon realized Sells wasn’t “your typical marketing guy.”

When the OCC came knocking later that year to insist that Quontic quickly change its deposit mix — Schnall said it was required to reduce its dependence on wholesale funding and attract significantly more core deposits — he saw a new use for Sells’ skill set. Sells agreed to shelve his digital marketing business in Indiana and move to New York to work full time at Quontic.

Perhaps no one is more cognizant of the initial challenges Sells faced than Ben Ramharak, vice president of IT and security at the $395 million-asset Quontic.

Ramharak has worked at the bank since 2005 — four years before Schnall, who had been a real estate developer and founded a national mortage banking company, acquired the flailing Golden First Bank during the financial crisis, moved it from Great Neck to Astoria, and changed its name. (Sells was in seventh grade when Ramharak took that job.)

Ramharak admits to being in the camp of those who gave “big time” pushback to Sells’ progressive strategy. Sells seemed to question the status quo incessantly, down to the bank’s practice of depending on its core provider for generating reports. “I’m a traditional — I was a traditional IT banker,” Ramharak said, correcting himself midsentence. “From a cybersecurity perspective, I couldn’t dream about running APIs within our own environment. I wouldn’t even touch them.”

Yet before long Sells would have Ramharak helping oversee the creation of cloud-based middleware called Quontic.Works that would drastically reduce the time it took the bank to generate reports.

For that to happen, though, Sells had to first win hearts and minds. Ramharak gives him as much credit for that as for the digital strategy itself. “Patrick actually is the one that came in and not only worked on completely overhauling the bank’s digital presence, whether it be customer facing or even internal, but also changed the bank’s corporate culture 180 degrees.”

As part of the process, Sells devised a new mission statement: “To break the system for financial empowerment.”

“That’s a little provocative for a bank’s mission statement,” Sells admits, “but what we’re saying is we want to think differently about the financial system, kind of Apple-esque, with their ‘Think Different’ campaign.”

Borrowing a page from business gurus he admires like Patrick Lencioni, Sells then codified the new mission with four core values.

The first is “try it on.”

“Whenever we’re talking about new things we say, ‘OK guys, we’re going to try this on.’ And immediately somebody goes, ‘Well, that’s not how it’s always been done’ or ‘I don’t know about that’ or ‘That seems new.’ Hold on a minute — we’re just trying it on.”

The next is “progress, not perfection.” Given how highly regulated banks are, the tendency is to err on the side of being conservative in an effort to avoid errors at all cost, Sells said. “This weighted focus on perfection gets in the way of innovation and speed.”

It means most community banks approach technology in a way that feels too static to Sells. “You’re used to signing a five-year contract with your core provider, which means you’re using the same technology for five years, as opposed to this kind of constant evolution,” he said.

Read about our other 2020 Digital Banker of the Year honorees:

OceanFirst’s David Howard

Bank of the West’s Hisham Salama

Bank of America’s David Tyrie

Ramharak has come to appreciate Sells’ philosophy. “If we start on Monday with something and by Friday he realizes maybe that’s not the right course to go on, he’s able to be very agile about it and just change. And I think that is actually what has gotten this bank to be able to quickly adapt to certain things.”

The third core value, “know your goal,” helps weed out half-baked ideas by emphasizing the importance of using data to quantify results. Innovation doesn’t mean that anything goes. But it does allow for a margin of error — which is where the policy of failure came in.

Sells said the core values helped foster better teamwork. “We had to build a common language that could get everyone talking the same way.”

This effort also entailed creating “key performance indicators” for everyone in the bank — which Ramharak says was entirely new for Quontic.

A regular cadence of staff meetings to improve communication and measure progress further helped get people in sync. “Everything is very focused and better organized now,” Ramharak said, “as opposed to the past, where it was just one end of the bank could be doing one thing and the other end didn’t understand it.”

Individuals started to get how their roles fit into the bigger picture and how their efforts would be measured and rewarded. “To his credit, he really took on that initiative and championed it, and we’re moving a mountain culturally,” Schnall said.

How Sells is so capable at his age is “dumbfounding” to Schnall, who himself started his first business at 23. “I’ve often remarked that it seemed like magic how he is able to accomplish so much with so few years of experience,” Schnall said. “People twice his age look to him, not just for business guidance, but for moral support — when people have problems, they go to him.”

Ramharak suspects it’s because Sells is a “generous listener.” “Patrick is the kind of guy that just lets you speak and then maybe you might even have a good few seconds before he realizes you’re done. He doesn’t interrupt,” Ramharak said.

Scott Collins, a senior product manager at Amazon, thinks of the several years he spent at Sells’ digital marketing agency as a “high-water mark.” He said Sells holds other people to the standards he sets for himself, which can be both exciting and demanding for those on his team.

“He comes up with big ideas then has the brain power and wherewithal to actually make them happen. So it was kind of ever-changing because he’s excited about a lot of different things,” Collins said.

Both Ramharak and Collins also described Sells as affable, which might have influenced Quontic’s fourth and final core value: “Say cheese.”

With smiling for the camera as mnemonic, the idea is to bring joy to customers by helping them financially and to have fun while doing it.

Because “it can be stressful when you’re changing,” the importance of getting people to smile should not be underestimated, Sells says.

“Those core values really are the ingredients that I think allowed us to change the culture and ultimately live out our mission statement.”

Change at the core

As Sells was trying to shift the team mindset in those early months, the bank’s back-end operations needed attention — quickly. With the pressure of the OCC agreement, there was no time to wait for everyone to come around. Changes had to proceed.

At its core — pun intended — Quontic was operating like a typical community bank, running on FIS’s Horizon platform, with online and mobile banking systems layered in. It also used Ellie Mae’s Encompass mortgage software.

“The systems didn’t talk to each other, so it required a lot of man-hours to be able to extract usable data from each of these systems and build reports around them,” Schnall said.

Quontic has been a certified CDFI for roughly five years — in 2019, 70% of its mortgages went to lower-income borrowers, according to Sells — and reporting was especially onerous for those activities. “We’ve had highly compensated people spending way too much of their time on this,” Schnall said.

Upgrading to a different core was not an option: too time- and resource-intensive. A middleware solution was in order, which presented another challenge. There was not a single programmer among the half-dozen members of the IT team. Though he has since learned that few community banks have one, Sells says, “this was something that really caught me off guard when I came to Quontic.”

“We’re moving a mountain culturally,” says Quontic CEO Steven Schnall of the bank’s digital transformation.

At that point Quontic partnered with the Canadian firm HubOne to create a custom accounting and document management system running on Microsoft’s Azure cloud computing service. Now Quontic can port in data from the various programs across the bank and, with the help of custom APIs, generate in minutes reports that used to take a week or more.

“We’re literally able to push a button and have all of the data reported to us complete with charts and graphs, as well as the extract of the data file behind it,” Schnall said.

Another key benefit is that the Quontic.Works system, which launched in June 2019, makes integrating new technology from partners far easier and more efficient, Sells added.

Quontic.Works is more typical of a large bank than a small one, said Craig Focardi, senior analyst at Celent.

“It’s a great strategy for balanced growth at a low cost,” he said. “They can better control their own destiny with how much additional tech functionality they can roll out to their customers, because they’re determining the rollout timeline, not their core vendors.”

Every employee has a login for Quontic.Works, where they can access real-time data to help with their jobs, along with task lists from managers.

“If you’re in the branch, here’s some customers that maybe need some follow-up on something,” Ramharak said, describing one way that employees use the newly available insight. “We’re going to be able to put all of these data sources together and make a specific dashboard based on the employee’s role and responsibilities.”

Retail (deposit) therapy

Quontic’s customer-facing technology also got an overhaul last year, as the bank urgently worked to attract more retail deposits.

Within 30 days of Sells’ arrival at Quontic, the bank deployed a solution from its core provider to enable a digital onboarding process for deposit products. It was not ideal — registration took about 10 minutes, causing too many people to drop off before they completed the process, Sells said.

But offering the ability to sign up online, along with a high-yield savings promotion, supercharged new account activity so much that Quontic, which had no call center, needed a way to handle an influx of customer service calls.

One of the bank’s executives mentioned that his daughter, an aspiring actor, was in search of a job with flexible hours. She recruited her friends, and in short order a group of 30 New York actors had become temporary Quontic reps in rented WeWork office space, tiding the bank over for most of last year until it could set up and staff a call center. “Customers absolutely loved talking to those people, as opposed to your typical bank call center staff,” Sells said.

Even so, Sells was determined to shrink the number of people seeking customer service help.

In June, Quontic switched to an identity verification solution from Jumio, which cut registration times by several minutes. And this spring, with the help of the tech firm Mantl, the bank improved its online account opening process again, cutting the time to sign up to three minutes.

Now, more than 95% of Quontic customers onboard digitally and customers come from all 50 states. Conversion rates have jumped 150% while customer acquisition costs have dropped by 90%. And none of the efforts to capture more deposits involved adding brick-and-mortar locations, a savings that helps fund the tech budget, Schnall said.

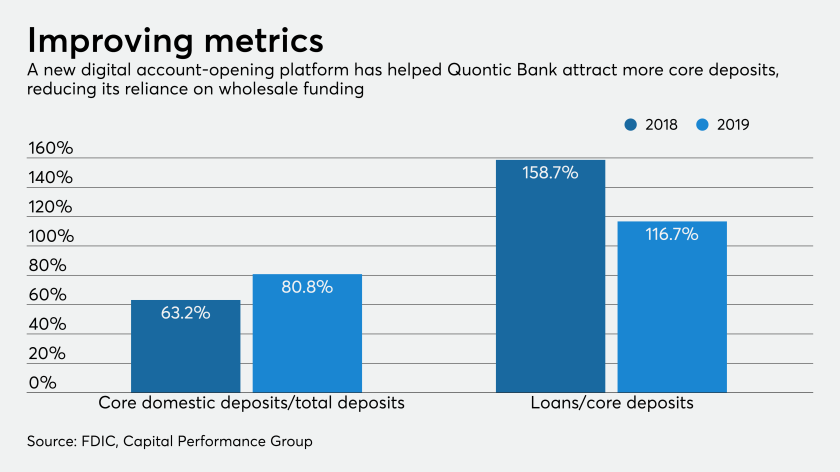

But perhaps most important, data from the Federal Deposit Insurance Corp. suggests Quontic’s efforts to shift its deposit mix have been successful.

At the end of 2018, brokered deposits made up about 34% of Quontic’s total deposits, with core deposits at 63%, according to an analysis of the data by Capital Performance Group.

By the end of last year, brokered deposits had shrunk to below 3%, with core deposits rising to about 81%. Its overall deposits totaled $318.9 million, up 1.6% from the year earlier. Meanwhile, its loan-to-core-deposit fell from nearly 160% at the end of 2018 to about 117% at the end of 2019.

Its next phase of deposit growth involves a new program called QuonticMax, which the bank launched in beta in January and began marketing in May. The brokered money market, checking and savings accounts target rate-conscious, high-net-worth customers.

The QuonticMax offering functions like a single account to the customer, but spreads funds in $250,000 chunks across partner institutions to provide FDIC insurance up to $160 million.

Many banks opt not to market this type of service, for fear of cannibalizing large accounts, Sells said. But that is not a concern for Quontic. “We don’t have hundreds and hundreds of millions of dollars in customers’ balances that are over that insurance limit that we would be losing. So if we brought in a new customer specifically tied to this, their $250,000 that we would keep is an incremental $250,000 for us,” he said. “The fact that another $5 million, $10 million, would go somewhere else doesn’t hurt us.”

Since the soft launch in the first quarter, QuonticMax has generated more than $76 million in deposits, Sells said. Over time the bank aims to attract more than $200 million through that offering.

Wearables, crypto and the future

One of the reasons Sells and Schnall clicked was their mutual interest in cryptocurrency. Their conversations seeded an idea: What if they could create a consumer deposit product tied to cryptocurrency? “We’ve been working very hard with our regulators to come up with a structure that will be fully compliant with all laws and regulations and we believe we’re getting close,” Schnall said, declining to share details.

Though some might think of it as a niche product, Schnall contends that cryptocurrency has wide appeal, with enthusiasts among young and old, high-net-worth and low-income. “The market for that product crosses all demographics,” he said.

Other tech-forward plans include a ring with the functionality of a contactless debit or credit card. Schnall aims to make this low-cost wearable device available to all deposit customers but is looking to target niche audiences in particular — mass transit users in large urban centers, outdoor enthusiasts and extreme athletes. Quontic has more than 2,000 customers on a waitlist for the product and Sells is one of them.

“I’ve been an ultra-marathon runner for quite a while and, if I’m going on a 30-mile run, I’m not going to bring

a phone or money with me,” Sells said. “But I may want to stop at a Duane Reade or something and get a

Gatorade.”

Schnall would relish being able to wave his hand at a turnstile to pay for his morning commute. “I ride the subway to work and I typically have a cup of coffee in one hand and something else in another hand,” he said.

The launch has been pushed back due to the coronavirus outbreak, but they hope to get the ring out in the next few months. “We think it’s a good story consistent with our being a digital bank,” Schnall said. “While it’s not going to be for everyone, it’s for some people.”

The volume of payments made via wearables is growing, but most of the activity is through key players like Apple and Fitbit, said Emmett Higdon, director of digital banking at Javelin Strategy & Research.

Still, in Higdon’s view, Quontic’s tech forays are a differentiator. He pointed out that Quontic also offers Zelle, which he said is “very unusual” for a community bank.

But he questioned how long Quontic could sustain its strategy of offering high yields on its online accounts. “They seem to be cherry-picking certain aspects of the market and at least at the surface doing a very fine job of it to be able to pay out the rates that they are on their savings accounts. Does that lead to durable, very sticky, loyal relationships with those customers? Not necessarily,” Higdon said.

Schnall shrugs off this concern, saying that he believes working with consumers at both ends of the spectrum — offering mortgages mainly to lower-income individuals and gathering deposits from higher-income segments — will continue to be an effective strategy. “Anything that we could do on the deposit side to drive low-cost deposits to scale enables us to do more on the lending side for our target market,” which is primarily low-income communities, he said.

Most of Quontic’s lending had been local before Sells’ tech initiatives allowed it to begin offering mortgages outside of its home market in June 2019.

Since Sells’ arrival, the bank has spent $3 million on tech efforts overall. “For us, it was massive; we spent less than $1 million a year before,” said Sells, who, as an essential employee in the financial services sector, has continued to go into Quontic’s headquarters at Rockefeller Center to keep the momentum going, even as New York’s stay-at-home orders this spring shuttered many businesses and left Manhattan streets deserted.

Quontic plans to invest another $2 million in the next 18 months to further develop its tech strategy.

Sells sees that spending commitment as a great opportunity to bring fresh thinking to community banking. “A lot of people who work in banks are lifelong bankers, and business has always been done a certain way. There’s a certain approach to it,” he said.

That means coming in with new ideas is a lot like trying to plant seeds in concrete — if you don’t get the ground ready, the effort will fail, regardless of support from top executives.

That’s why, Sells says, “innovation couldn’t just be coming from Steve or I, it had to live in the whole bank.”

Community bank CEOs he comes across at conferences often don’t get this, he says. “They’ll say, ‘We hired one tech guy to help us and we’re going to become innovative.’ Well, one person is not going to be able to change a multi-hundred-person organization,” Sells insists. “You have to get this instilled culturally.”

Schnall agrees with that assessment. But at the same time, Schnall says, he can give one person credit for making some difference in Quontic’s case, at least in terms of being a catalyst for change.