Awards

Awards

Alkami and MANTL Named to American Banker’s 2025 “Best Places to Work in Fintech”...

Awards

MANTL Named One of American Banker’s “Best Places to Work in Financial Technology” in...

Awards

MANTL Honored by Goldman Sachs for Entrepreneurship

Awards

MANTL Named “Best Place to Work in Fintech” by American Banker

Customer News

Customer News

Amplify Credit Union Partners with MANTL to Modernize Business and Retail Account Opening

Customer News

The Atlantic Federal Credit Union Becomes First Credit Union to Go Live with MANTL...

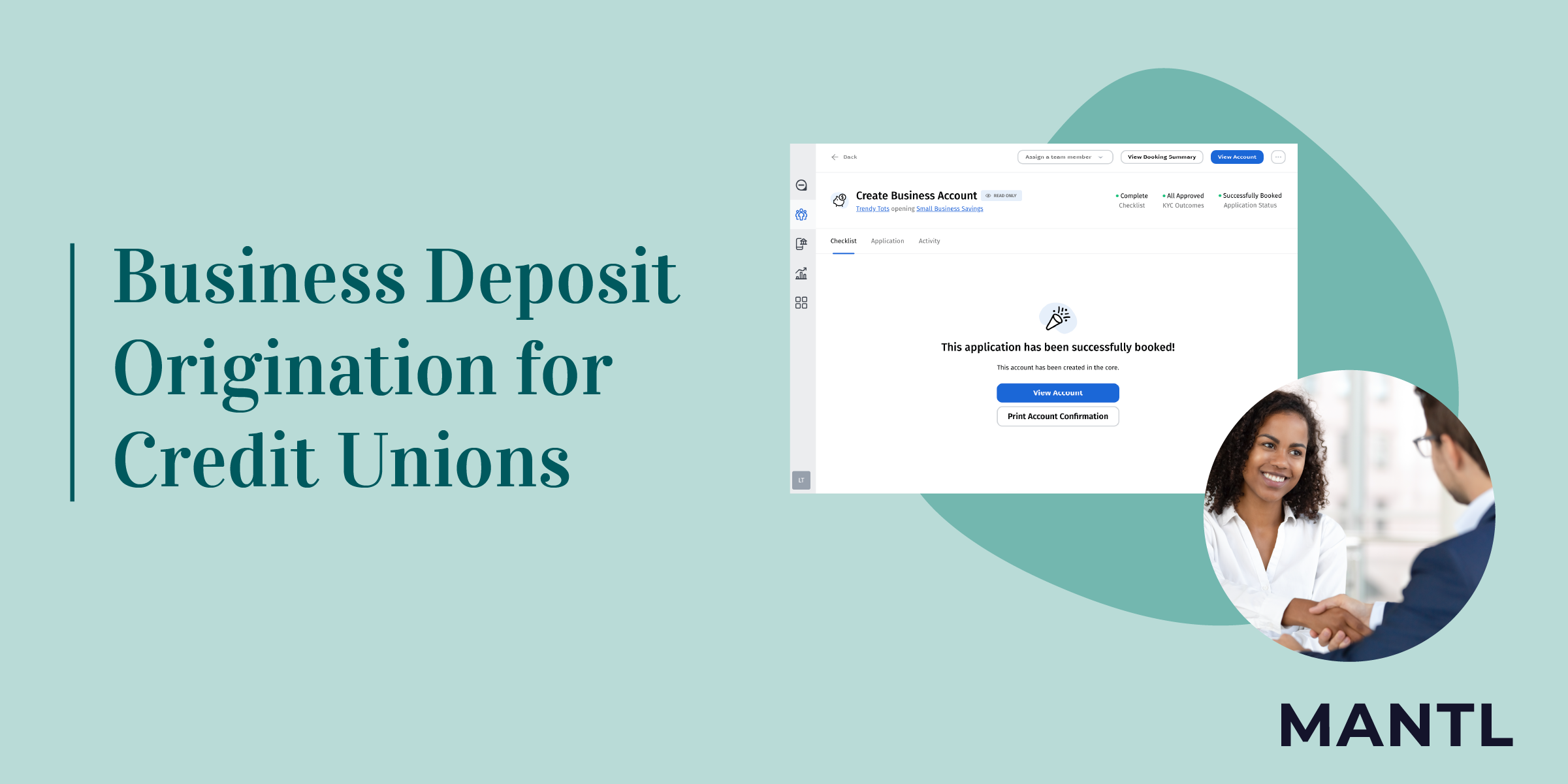

Credit Union

Loan Origination

Products & features

Customer News

Grow Financial Credit Union Chooses MANTL to Elevate the Member Experience

Credit Union

Products & features

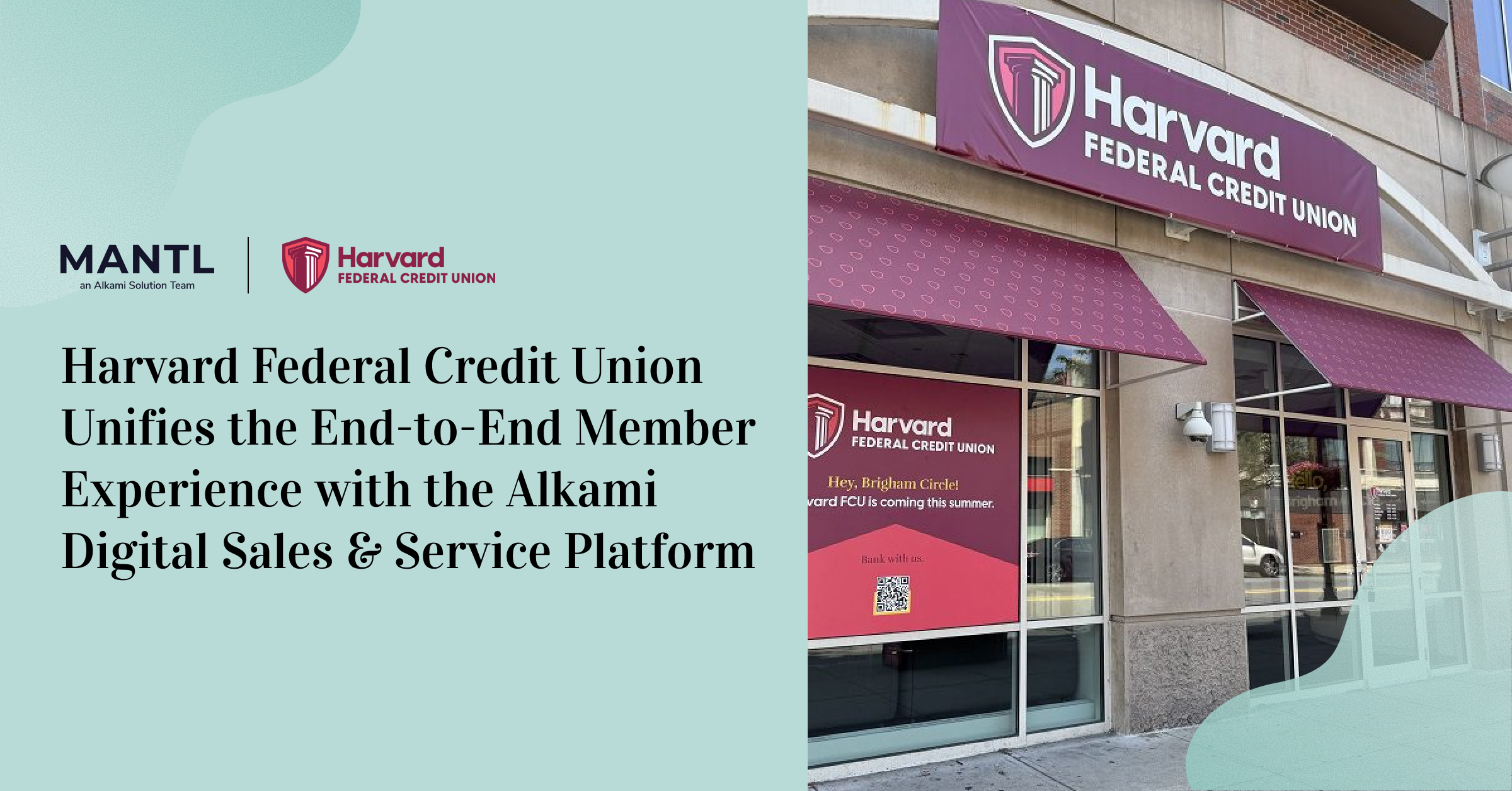

Customer News

Harvard Federal Credit Union Unifies the End-to-End Member Experience with the Alkami Digital Sales...

Credit Union

Products & features

MANTL News

MANTL News

MANTL Expands Platform to Create All-in-One Solution for Deposit and Loan Origination

MANTL News

The MANTL–Alloy Partnership Surpasses 2 Million Processed Applications

MANTL News

MANTL Partners with Method Financial to Modernize Loan Refinancing with Real-time Liability Data Integrations

MANTL News

Financial Plus Credit Union Wins “Most Effective Technology Implementation” Innovator Award for Transformative MANTL...

Digital transformation

Loan Origination

Products & features