How can MANTL optimize your deposit raising?

Financial Institutions across the nation are stepping up their efforts to raise consumer and commercial deposits. Here’s how MANTL sets you up to win.

1

Leveling out Loan-to-Deposit Ratio

With rising interest rates, people and businesses are cutting ties with long held deposit relationships in pursuit of high-yield offerings. The increased competition means banks need the right technology and strategy in place to meet their deposit goals and level out their LTD Ratio.

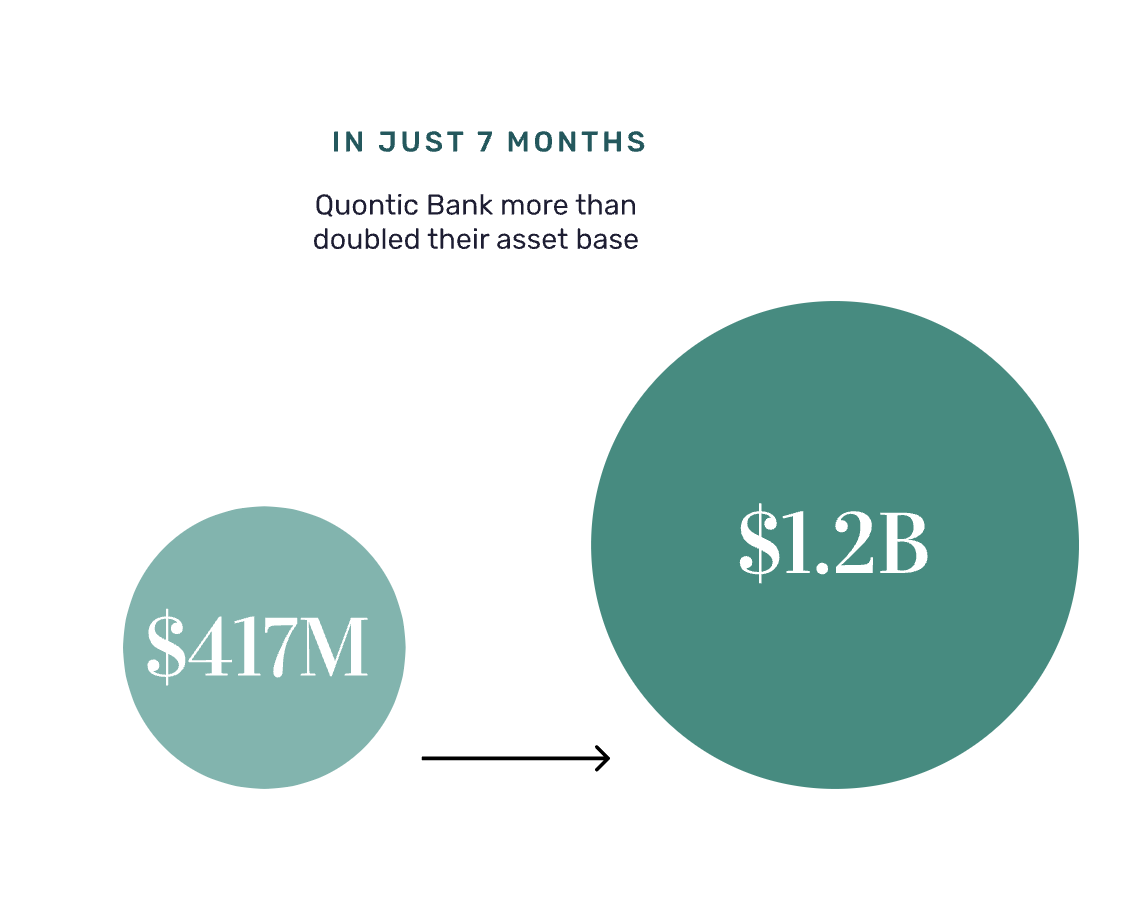

After becoming a MANTL customer, Quontic Bank more than doubled their asset base — from $417 million in assets to $1.2 billion — in just 7 months while facing regulatory pressure to raise deposits. Ultimately, it’s the banks offering frictionless omnichannel digital account opening experiences that will be on the winning side of the deposit war.

2

Swapping Wholesale Funding for Core Deposits

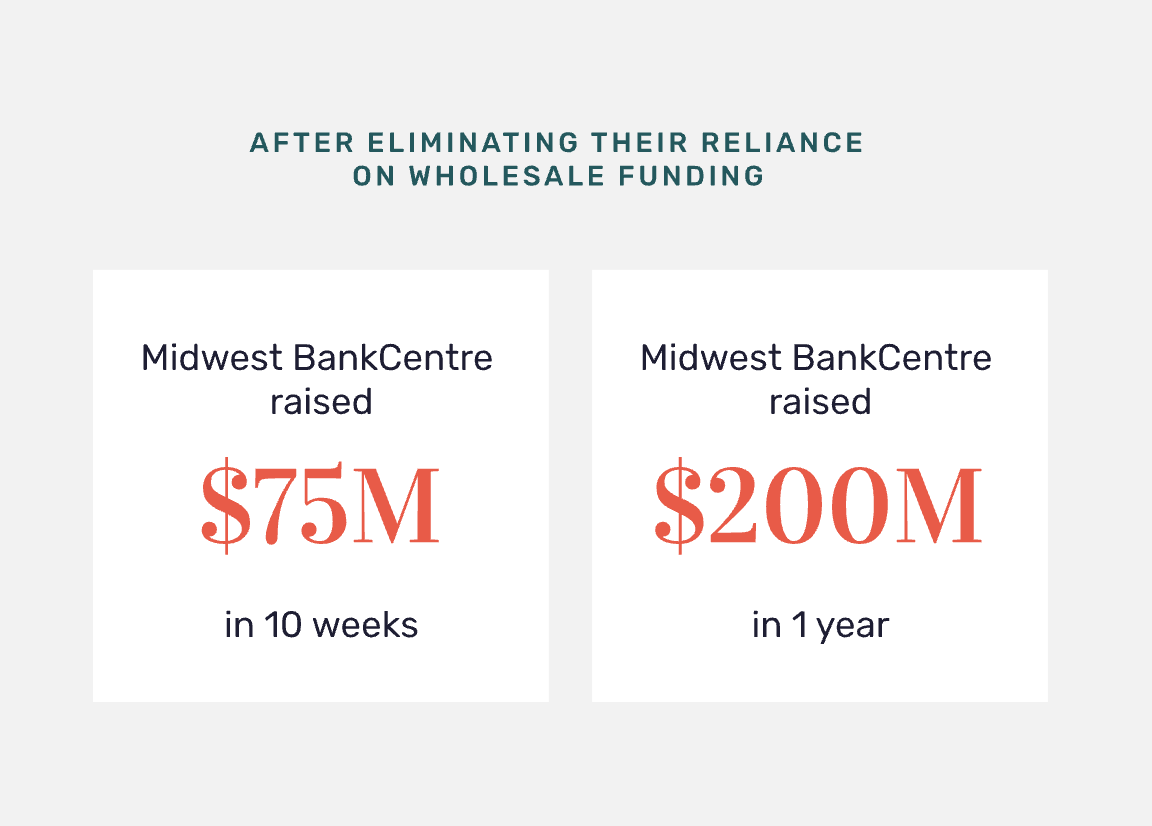

As the overnight bank funding rate climbs above 4.5%, banks can no longer rely heavily on wholesale funding to add liquidity to their balance sheet. But, with the entire market stepping up their efforts to raise core deposits, winning them won’t come easy. In 2019, MANTL worked with Midwest BankCentre to eliminate their reliance on wholesale funding, helping them raise $75 million in 10 weeks and $200 million in the first year.

3

Improving operational efficiency

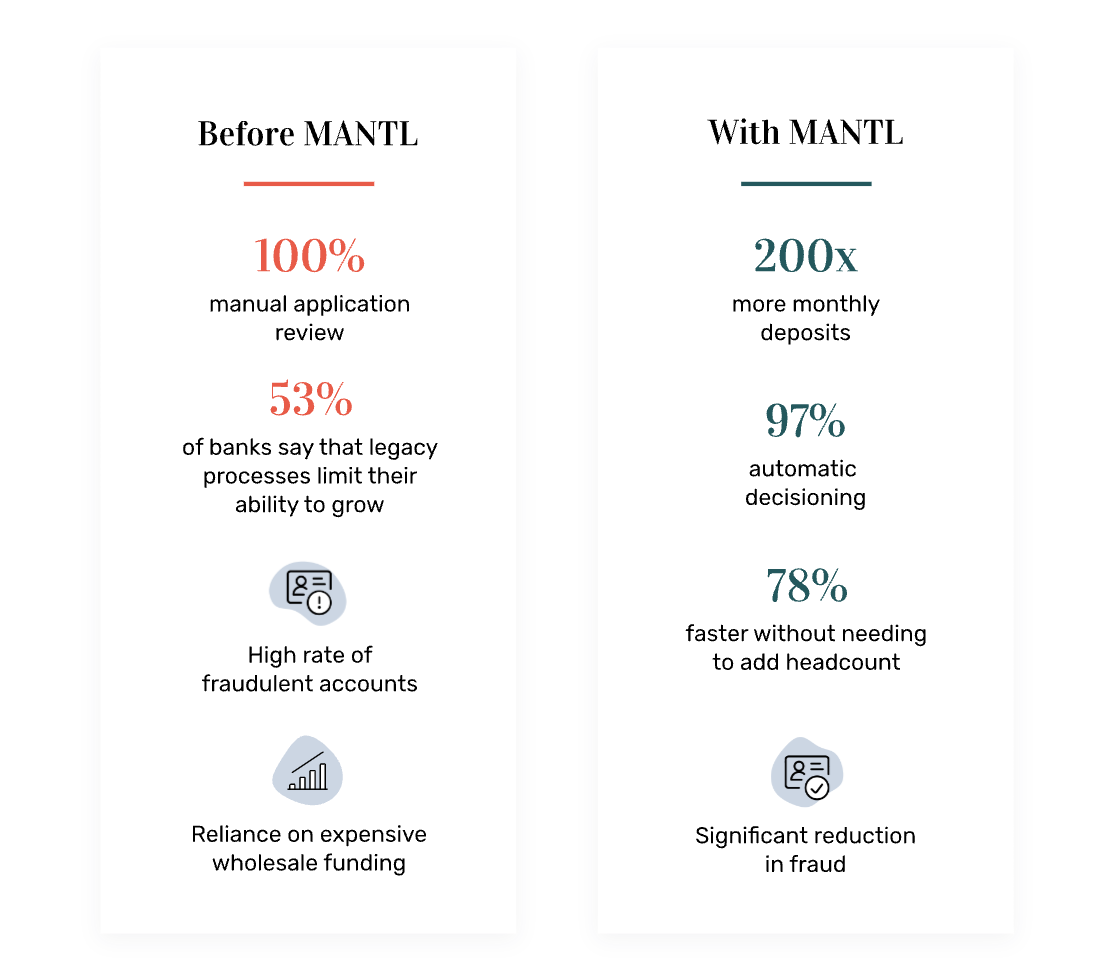

Inflation is at a forty-year high and banks can’t afford to have excess waste from inefficient account opening operations. By maximizing your application’s conversion rate and reducing manual operational tasks, banks can effectively capture the demand in their local markets or expand nationwide without the need to increase headcount. In fact, we’ve seen banks manage 10x their pre-MANTL volumes with no additional staff.

A high-performing deposit origination solution not only increases operational efficiency for your staff, but also makes the account opening process seamless for your customers. Take it from Horicon Bank, which originated 20% more checking accounts each month at a lower cost, with no additional headcount.

Working with MANTL has resulted in the same deposit growth as building 10 new branches.

Dale Oberkfell

President & CEO

Midwest BankCentre